Your credit score is more than just a number. It quietly affects a lot of real-life decisions, from getting approved for a loan to how much interest you might end up paying. In many ways, it’s also tied to your overall financial wellness, because it reflects how you manage money, bills, and debt over time.

If you’ve ever felt unsure about where you stand or what’s hurting your score, you’re not alone. The good news is that it’s something you can improve step by step. In this guide, we’ll walk through simple, practical credit score tips in Australia that can help you build better financial habits and strengthen your financial wellness along the way.

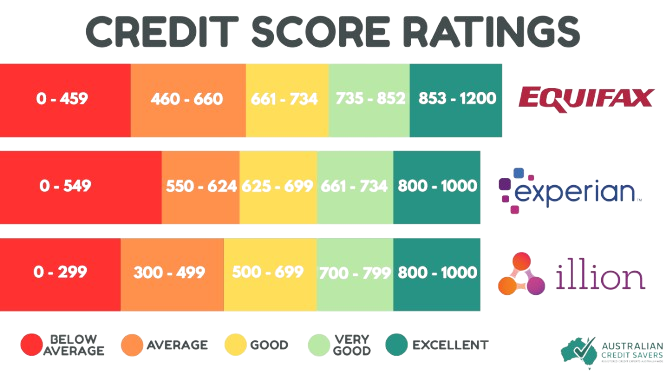

Understanding Your Credit Score In Australia

In Australia, a good credit score typically ranges between 500 and 734, depending on which credit bureau you use, with higher numbers indicating better creditworthiness. The three major credit reporting bodies (Equifax, Experian, and Illion) each use slightly different scoring systems, but all serve the same fundamental purpose: helping lenders assess your risk as a borrower.

Your credit score influences everything from mortgage approvals to mobile phone contracts. A strong score can save you thousands of dollars in interest over the life of a loan, while a poor score might limit your options or result in higher borrowing costs.

The Five Key Factors Affecting Your Credit Score

Payment History

This is the most significant factor in determining your creditworthiness. Late payments, defaults, and bankruptcies can severely damage your score and remain on your credit report for several years. Pay all bills on time, every time. If you have multiple credit cards, consider the “avalanche method” where you pay the minimum amount on all cards while directing extra payments to the card with the highest interest rate. If you want a more structured approach, you can learn other strategies to pay off debt faster that can help you manage repayments more effectively.

Credit Utilisation

This measures how much of your available credit you’re using. Keeping credit card balances below 30% of your credit limit demonstrates responsible credit management.

Length of Credit History

Longer credit histories generally result in higher scores, as they provide more data about your borrowing patterns. Unless there’s an annual fee involved, keep your oldest credit accounts open.

Types of Credit

Having various credit types like credit cards, personal loans, and mortgages can positively impact your score. Keep in mind, however, that more accounts don’t necessarily mean a better score; consistent, on-time payments are what truly matter.

New Credit Inquiries

Multiple credit applications in a short period can temporarily lower your score, as it may indicate financial stress or hardship. Only apply for new credit when absolutely necessary, and space out applications by at least six months when possible.

Building Broader Financial Wellness

While your credit score is crucial, true financial wellness is built on a solid approach to money management. Here are essential strategies to strengthen your overall financial position.

Create and Stick to a Budget

Use the 50/30/20 rule as a starting point: allocate 50% of after-tax income to needs, 30% to wants, and 20% to savings and debt repayment. Modern budgeting apps can automate much of this process, tracking your spending patters and alerting you when you’re approaching budget limits.

Build An Emergency Fund

Aim to save at least three to six months’ worth of living expenses in a separate but readily accessible account. It is completely okay to start small! Even $500 can cover many unexpected expenses and prevent you from relying on credit cards during emergencies. Try to save first before spending.

Review and Optimise Your Subscriptions

One of the most overlooked expenses are subscriptions. Conduct a monthly audit of recurring payments and subscriptions. Cancel services you don’t actively use, and consider downgrading others. Many people unknowingly pay for multiple streaming services, gym memberships, or software subscriptions they rarely use.

Taking the Next Step Toward Financial Wellness

Building strong financial wellness takes time, patience, and a more complete approach than just focusing on your credit score alone. While improving your credit score can open doors to better loan options and financial opportunities, true financial wellness comes from developing consistent money habits, managing debt wisely, and gradually building financial stability that lasts.

Sometimes, even when you’re doing everything right, your credit score may not improve as quickly as you expect. If that happens, it may be worth getting expert support to understand what’s really holding your report back and what can be done to fix it.

That’s where we can help. Through our credit repair services, Australian Credit Savers works with you to identify negative listings, review your credit report in detail, and create a clear plan to help improve your credit profile over time.

If you’re ready to take the next step, don’t wait for things to get worse. Contact us and get a free credit review today, and find out what’s affecting your score, and what you can do about it.