If you’re trying to rebuild your credit, every choice with your finances matters. A low-rate credit card can be a great way to start. These cards usually have smaller interest rates, fewer fees, and easier-to-understand terms. That makes them a good option for anyone who wants to pay off debt more easily and slowly improve their credit score.

In Australia, you can find plenty of low-interest credit cards, each made to fit different budgets, lifestyles, and financial goals. Whether you’re after a card with no annual fee, a low-cost credit card that helps you save on interest, or a low-interest credit card for good credit, knowing your options can make a big difference.

Why Low-Rate Credit Cards Are Ideal For Credit Repair

If you’re currently repairing your credit, a low-rate credit card can be your best ally. High-interest credit cards can make it tough to pay off your balance, especially if you’re carrying debt monthly. When the interest keeps adding up, it feels like you’re paying but not really getting anywhere.

A low-rate credit card can help ease that pressure. Since you’re charged less interest, more of your money goes toward paying down what you actually owe. It’s a small change that can make a big difference over time.

These types of cards can also give you more breathing room to stay consistent with your payments. Paying on time shows lenders that you’re responsible with credit. As you keep that habit, your credit score can slowly improve, giving you better chances for loans or other financial products in the future.

But using a card with low interest isn’t just about the rate itself. It’s about setting up a habit of managing money carefully and using credit strategically instead of impulsively.

But First, How Do Credit Card Interests Work?

Every credit card has what’s called an annual percentage rate, or APR. This is the interest you’re charged when you don’t pay your full balance. If you pay everything off each month, you won’t have to worry about interest at all. But once you leave part of your balance unpaid after the due date, interest starts to build up every day.

For instance, if you owe $1,000 on a card with a 20% rate, you’ll end up paying around $200 in interest over a year if you don’t clear it. On the other hand, a low-rate card with a 10% APR would cut that amount in half. It’s a small change, but it can make a big difference when you’re trying to stay on top of your payments.

This is why low interest credit cards are particularly powerful for people in credit repair. They’re not a quick fix, but they make it easier to manage repayments and avoid debt piling up. With time and consistent effort, they can help you move toward better financial stability.

What To Look For In A Low-Rate Credit Card

When comparing low interest credit cards, focus on more than just the advertised rate. While the lowest interest credit card might seem like the best deal, it’s important to consider other features that can impact your long-term costs.

Ongoing Interest Rate

Check whether the card offers a promotional rate or a permanent low rate. Some cards start with an introductory offer that increases after a few months, while others maintain a low rate consistently. For credit repair, a steady low rate is usually better.

Fees And Charges

Look for no annual charges or low annual fee credit cards. If you’re rebuilding your credit, minimizing fees helps you focus on repayments instead of extra costs. Some providers also offer zero fee credit cards or cards with no annual fee, which can be perfect if you don’t use the card often.

Rewards And Extras

Although rewards might not be your top priority right now, some no fee credit cards with rewards can offer cashbacks or points on everyday spending. Just make sure these rewards don’t come with higher interest or hidden costs.

Credit Limit

A modest limit can help you control spending while demonstrating responsible use. Over time, your credit limit can increase as your score improves.

Benefits Of Choosing A Low Interest Credit Card

A low-cost credit card is not just about saving on interest. It’s a strategic move to rebuild your financial reputation. Here’s why these cards make sense for Australians working on their credit repair journey.

Easier Debt Management

Lower interest means smaller repayments if you ever carry a balance. This helps you stay consistent and avoid missed payments, which can damage your credit history.

Financial Flexibility

A low-rate credit card can act as a safety net for unexpected expenses without burdening you with heavy interest charges. For instance, if your car needs repairs or a medical bill comes up, you can pay it off over time without being penalized with high rates.

Improves Credit Behaviour

Each on-time payment contributes to a better credit record. Even small, consistent repayments can steadily raise your credit score.

Fewer Fees, Fewer Surprises

Cards that charge no annual fee or offer low-cost structures are easier to maintain. When you’re trying to recover financially, every dollar saved helps.

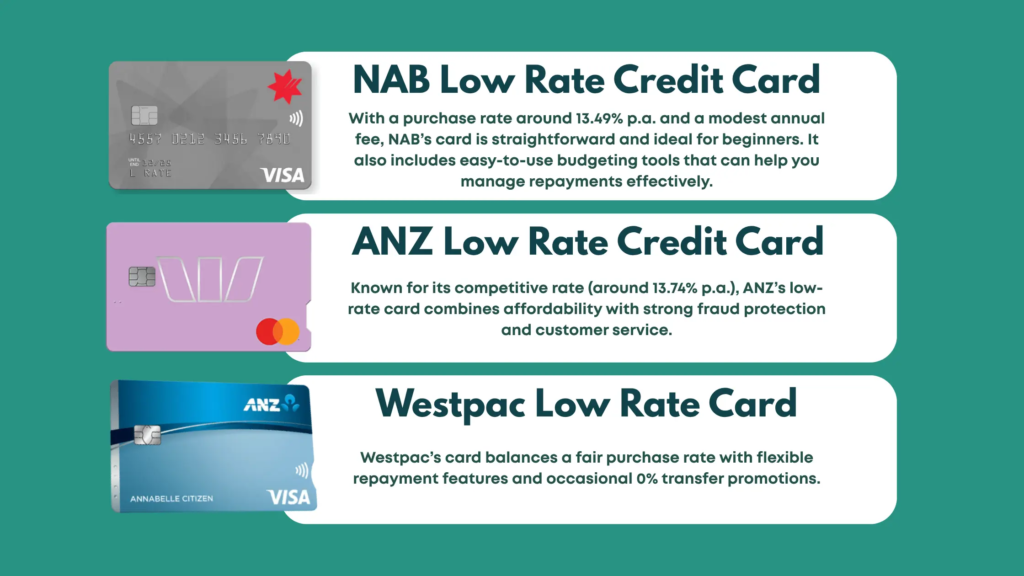

Popular Low Interest Credit Cards

These examples are intended to provide general information and do not constitute a recommendation or endorsement. Individuals are encouraged to review the official bank websites or trusted comparison platforms for the most current rates and terms.

Using A Low-Rate Credit Card Wisely

The card itself doesn’t rebuild your credit; your behaviour does.

Use your card for manageable and recurring purchases like groceries, fuel, or streaming subscriptions. Pay them off monthly. You can even set automatic payments or calendar alerts. Ideally, use less than 30% of your credit limit. For a $1,000 limit, that means staying under $300.

Check your credit report regularly through credit reporting agencies like Equifax or Experian. Tracking your improvements can keep you motivated. Australian Credit Savers offers a free credit report assessment to help you assess where you stand with your credit profile.

Choosing What Fits Your Situation Best

The best low-rate credit card depends on where you are in your financial recovery. However, it’s also important to remember that even applying for a low-interest credit card will create an enquiry on your credit report. Too many applications can make lenders see you as a higher risk. So it’s still best to do your own research first, choose one card that fits your needs, and avoid applying for several at once.

Whatever you choose, remember that the goal isn’t to rely on credit; it’s to use it as a tool. Small, consistent purchases and timely payments demonstrate reliability to future lenders.

At Australian Credit Savers, we help review credit reports for inaccuracies, identify outdated or incorrect listings, and dispute them for you. By combining professional credit repair with responsible card use, you can rebuild your credit and increase your chances of being approved for loans, mortgages, or other financial products with more favourable terms.

Building A Strong Financial Foundation

Credit repair doesn’t happen overnight; it’s a process of rebuilding trust, one payment at a time. A low-rate credit card isn’t a shortcut, but it’s one of the safest, most effective tools to help you stay consistent and avoid the traps of high-interest debt.

The goal isn’t just to have credit again. It’s to manage it differently, using low-cost, transparent financial tools that work for you, not against you.

Whatever card you go for, what matters most is how you use it. With consistent payments, low balances, and smart financial habits, you can repair your credit score.